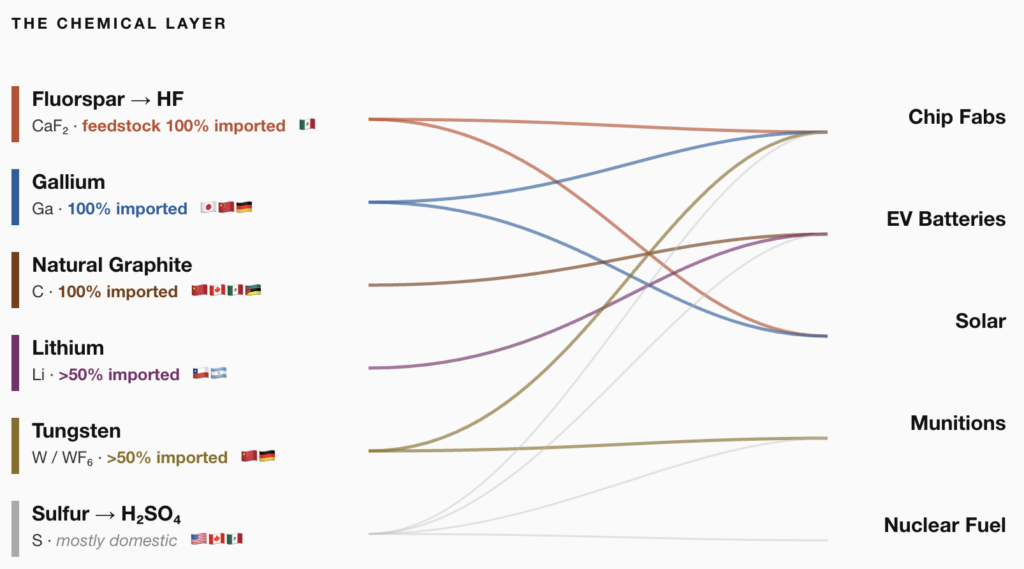

One of our more under-discussed, industrial-base bottlenecks seems to be: chemical processing. At $673B annual revenue, the U.S. has one of the largest chemical industries on earth (hey, that ain’t nothing!) — but it’s a volume industry of polyethylene, ammonia, chlorine (~98% pure) for plastics, fertilizer, and water treatment.

What fabs and gigafactories need is something different: purification chemistry. Hydrofluoric acid distilled in quartz-lined vessels to 99.9999% purity. Lithium recrystallized to electrochemical spec. Solvents cleaned to parts per trillion. Closer to pharmaceutical manufacturing than petrochemicals — and while the US has some domestic capability here, it’s not at the scale the buildout assumes. For the key feedstocks that enter these processes, we’re highly import-reliant.

All megaprojects, gigafactories, fabs, and rearmament production lines share one assumption: the chemical inputs will be there. While some sector-specific funding is out there — hundreds of millions of dollars flowing through DPA Title III into munitions‑related chemicals, and up to $325 million in CHIPS funding for Hemlock’s polysilicon capacity — we don’t have a holistic program focused on purification as a shared, cross-cutting layer underneath it all. For chips alone, McKinsey estimates ~$9B in chemical supply chain investment needed, with ~$4B still unfunded. Japan, Germany, and South Korea already have a lot of this at scale. The Renaissance, for now, runs on allied chemistry — which is much better than, say, the rare-earths situation.

If you are an American chemist living this daily, we want to hear what you are seeing: 💌 team@peraspera.us